Citator

What is a Citator?

A citator is a book, or set of volumes, that allows you to determine the history of a case and to evaluate the strength of its holdings. In a judicial system that relies heavily upon precedent (principles that were established in previous cases) it is important to be able to trace the establishment of a judicially derived point of the federal tax law. Citators can be used to determine the history of a judicial decision and how that decision has been criticized, approved, or otherwise commented upon in other court decisions. This type of information is also available for revenue rulings, revenue procedures, and certain other administrative pronouncements.

In general the case that is being analyzed is identified as the "cited case," and the later opinions that refer to that case are known as the citating cases. Cited cases are listed alphabetically, followed by the citing cases and rulings. The history of a cited case refers to all other decisions by higher or lower courts in the same case. For example if the case has been appealed to a higher court, the citator provides the name of the appellate court and whether it affirmed, reversed, or modified the decision of the cited case. Similarly, if the cited case is an appellate court decision, the citator provides the name of the trial court and states whether the cited case affirmed, reversed, or otherwise modified the decision of the lower court.

Citators also provide citing references, which provide other rulings or court cases that have discussed the cited ruling. You can also find information in a citator about how the decision of the cited case has been interpreted by other courts. These courts can, in their decisions, agree or disagree with the cited case, differentiate the facts or law in their case from the cited case, or may simply refer to the cited case without comment. Some citators use abbreviations to indicate which of these reasons are specified by the citing courts. For Revenue Rulings, citators provide historical citations to related rulings that revoke, modify, or supersede the cited ruling and to any earlier rulings affected by the cited ruling. The citators most frequently used are Research Institute of America's (RIA) "Federal Tax Citator," which comes in a multi-volume set; and Commerce Clearing House's (CCH) two volume set.

The Commerce Clearing House citator is part of the annotated tax service, the Standard Federal Tax Reports. The main citator is contained in two volumes, Citator Volume A - M and Citator Volume N - Z. The main citator table is supplemented by the current citator table, an update service that is issued quarterly and is placed in front of the main table. The two tables refer to all of the federal income tax decisions that have been issued since 1913; federal estate and gift tax cases are cited in a separate volume. Certain court decisions that are no longer applicable, because of a change in the underlying statute, are included in the listing; however, such cases are indicated by a dagger symbol, and no citating cases are listed.

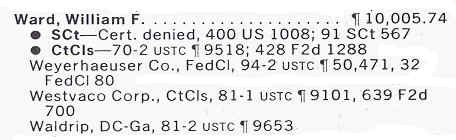

The following excerpt is reproduced from the CCH citator. Names of cited cases are set in bold print, followed by the paragraph reference(s) to the CCH tax services where the cited case is discussed relative to the code, regulations, and other pertinent court decisions. The bold dots that are placed along the citator's left margin facilitate a reconstruction of the judicial history of the cited case, with the highest level court to address the case first, and the trial level case listed last.

As you can see this case was brought to the Supreme Court but was denied a "writ of certiorari" (Cert. denied) which means that the Supreme Court did not hear the case. Listed below that is the trial level court, in this instance it was the US Court of Claims. Also included is the volume number (70-2) and paragraph (¶9518) where the case can be found in CCH's U.S. Tax Cases (USTC); and the volume (428) an page number (1288) of West's Federal reporter second series (F2d). The three cases listed after the Court of Claims decision are the citating cases. For a more complete discussion of the different types of courts and citations please see the "Judicial Sources" section.